The combined capital cities have risen by 2.5 per cent over the quarter and lifted by 1 per cent since the start of the month.

Dr Oliver estimates Sydney will rise by 1.7 per cent this month and the combined capitals by 1.3 per cent.

“It’s a pretty rapid turnaround. It seems that the shock of rate hikes has worn off and the shortage of supply has swamped the negative impact of higher interest rates,” he said.

There is a risk that the higher prices go up, the more the Reserve Bank will likely raise interest rates further to slow things down.

— Shane Oliver, chief economist, AMP Capital

Andrew Wilson, the chief economist at My Housing Market, also sees a potential double-digit growth in Sydney prices, based on the booming auction clearance rates.

“I think a 10 per cent increase is possible, given that we’re on the verge of an 80 per cent auction clearance right now, which is quite remarkable,” he said. “I think a lot of it is that buyers are realising home values are still lower than they were a year ago, but are now rising again.”

Eliza Owen, CoreLogic’s head of research, said if Sydney’s home values continued to rise by 1.3 per cent each month, as recorded in March and April, prices would climb by 13 per cent this year.

Sydney-based selling agent Thomas McGlynn of BresicWhitney said prices were likely to be stronger than the data was showing.

“Most sectors of the market are now actually performing quite strongly, even smaller apartments, so I think the price increases are not being reflected in the data yet,” he said.

“I think once the recent strong sales have flowed through, they’d show even stronger results.”

A similar calculation would see Perth values increasing by 5.1 per cent, Melbourne by 2 per cent and nationwide by 4.1 per cent.

“Demand for dwellings has seen an impressive lift in the past two months as evidenced by the increases in the CoreLogic Home Value Index, higher auction clearance rates, and a rise in the number and value of housing finance commitments reported by the Australian Bureau of Statistics,” Ms Owen said.

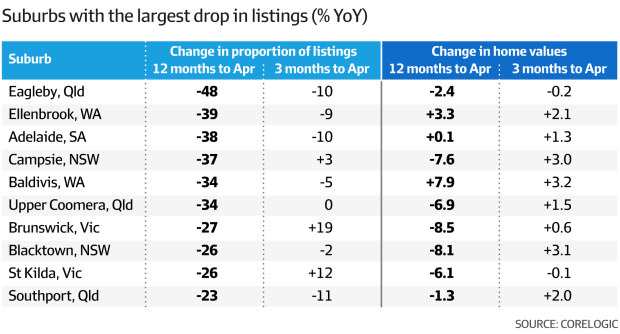

The rise in home prices could spark an increase in new listings nationwide as more vendors were enticed to list their homes, according to CoreLogic.

“At a high level, simple linear regression analysis suggests that for every 1 per cent increase in property values over the year, there is a 0.5 per cent increase in new listings in the same period,” Ms Owen said.

“This would equate to an increase in 2023 listings that was 2 per cent higher when compared to 2022. An additional 2 per cent on the 485,052 new listings over 2022, would equate to 494,753 listings over 2023.”

The total volume of dwellings for sale in Australia has been trending lower since the onset of COVID-19 restrictions in 2020.

As of April 2023, there were 138,144 homes listed for sale over the month, which is near decade-lows according to CoreLogic. At this level, total listings were 31.5 per cent below the decade monthly average, and 33.8 per cent lower than the average for April.

However, the assumption of 4.1 per cent capital growth nationwide this year, or a 13 per cent increase in Sydney prices remained highly uncertain, according to Dr Oliver.

“There is a risk that the higher prices go up, the more the Reserve Bank will likely raise interest rates further to slow things down,” he said.

“So there’s a risk the RBA will overdo the rate increases and the economy ends up with a recession at some point, which would be bad news for the property market.”

Ms Owen said the recovery was still in its early phase and there was no guarantee that the capital growth trend of recent weeks would continue.

“There is still some uncertainty around the trajectory for the cash rate, particularly given the latest monetary policy announcement showing a tightening bias from the Reserve Bank,” she said.

“Alternatively, there is a scenario that presents an upside risk for new listings. This would be a situation where vendors may need to sell their home, and not voluntarily.

“This may include households struggling to service a mortgage at higher interest rates, particularly amid rising unemployment over the course of the year.

“However, this scenario seems unlikely at present, given the low volume of new listings to date through rate rises, and strong pre-payment buffers across mortgaged households.“