“This benchmark for affordability shows that the vast majority of suburbs in the country’s capital cities are beyond this threshold, particularly for houses,” he said.

“This situation is particularly alarming for young people hoping to break into the housing market. With wage growth failing to keep pace with property prices, home ownership is increasingly slipping out of reach for younger Australians.”

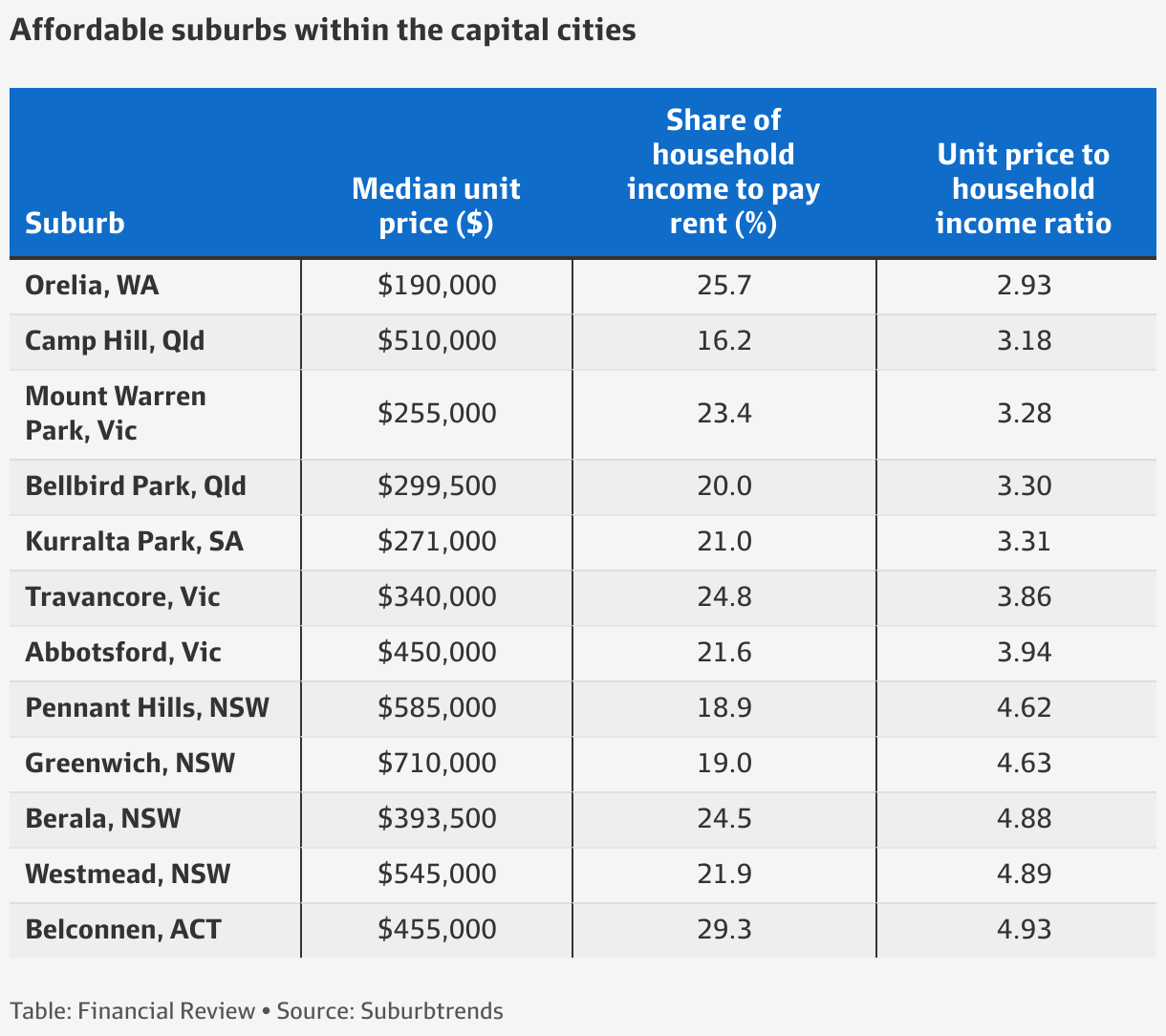

While unit markets were largely more affordable, only 13 suburbs in Sydney remained within the affordable range as incomes fell behind prices.

Units in Kellyville Ridge, Pennant Hills, Greenwich, Harris Park and Chipping Norton are among the most affordable, with the median values sitting around 4.6 times the suburb’s average annual household income.

Buyers in Brisbane have wider options to choose from with 65 per cent of all unit markets still priced within the affordable range.

Wilston, Camp Hill, Ashgrove and Paddington in Brisbane’s inner city are among the most affordable as prices stayed around $550,000 on average.

In Melbourne, 17 per cent of all unit markets, many of those in the inner city, are still within the affordable range. They include Travancore, Abbotsford and Windsor, where units are fetching between $340,000 and $450,000, which are around four times the average annual household income in these suburbs.

Across Canberra, units in 71 per cent of all suburbs are still affordable, 42 per cent of all unit markets in Adelaide and units in all suburbs in Darwin are priced within the affordable range. By contrast, all of Hobart’s unit markets were unaffordable.

“Without sufficient supply to meet demand, particularly for units, upward pressure on property prices will continue unabated, exacerbating the housing affordability crisis,” Mr Lardner said. “This will only deepen the divide between those who own property and those who do not, making it even more difficult for younger generations to achieve the dream of homeownership.”

Shane Oliver, AMP Capital chief economist said housing affordability has deteriorated massively since the 1990s.

“Prior to the mid 1990s average home prices ranged around two to six times annual wages but since then, it’s steadily increased to around 14 times,” Dr Oliver said.

“Similarly, the ratio of home prices to median household disposable income has blown out from around four times to eight times.”

The time it takes to save for a deposit to enter the property market has also ballooned to around 10 years, compared to around five years 30 years ago.

Dr Oliver said building more homes, relaxing land use rules, releasing land faster and speeding up the building approval process would help widen the pool of affordable homes.

In addition, matching the level of immigration to the ability of the property market to supply housing would also help.

“We have clearly failed to do this following reopening from the pandemic, and this is now evident in severe supply shortfalls,” Dr Oliver said.

Encouraging greater decentralisation to regional Australia is another potential option according to Dr Oliver.

“The work from home phenomenon shows this is possible, but it should be helped along with appropriate infrastructure and of course measures to boost regional housing supply,” he said.

“Policies that are less likely to be successful include grants and concessions for first home buyers as they just add to higher prices, and abolishing negative gearing which would just inject another distortion in the tax system and could adversely affect supply.”