“Interest rates are likely to rise further because inflation is still out there, so I want to wait and push back my plan to buy by around six months to see if more property owners will sell,” Mr Sebastian said.

“I think it’s simple mathematics. Interest rates are extremely high and people are probably stressed right now, or they’re just trying to hold on. But at some point, they’re going to have to sell, probably later this year or early next year, particularly if the RBA raises rates two or more times.

“Higher rates will also impact people’s borrowing capacity, so there will be less competition and more properties to choose from.”

Borrowing capacity ‘crunched’

The 12 rate increases have already slashed borrowing capacity by 32 per cent, according to RateCity research director Sally Tindall.

A home buyer earning $100,000 with a 20 per cent deposit and paying principal and interest with no kids or other debts can now only borrow $491,600. In April last year, they would likely have been able to borrow $722,700.

If interest rates increase to 4.35 per cent, this will drop to $481,000. If the rate hits 4.85 per cent, the loan amount will shrink again to $460,900.

“A handful of additional cash rate rises will crunch people’s borrowing capacity even further, but this alone is unlikely to cause property prices to plummet. An increase in stock, however, could change this equation,” Ms Tindall said.

“If the cash rate continues to climb, we could see an increase in stock over the second half of this year, as over-leveraged investors offload part of their portfolio and over-burdened families relocate to get relief from rising repayments.”

A homeowner 25 years into their mortgage and paying principal and interest on a $750,000 loan will now have to pay an extra $347 a month after Tuesday’s rate rise, according to RateCity. Since May last year, their monthly repayments have increased by $2049.

For those with a bigger mortgage, the latest rate increase added $463 to their monthly repayments, for a total of $2731 since rates started rising.

“Homeowners are likely struggling with their mortgages, but it’s not showing up in the overall data because so far, they’ve been able to refinance or get a better deal with their bank,” Dr Oliver said.

“But the more the RBA keeps raising interest rates, the less chance those people will be able to hang on without big cuts to their spending, possibly, unfortunately, having to sell their houses. So, there’s a growing risk here with each rate rise that comes along.”

Property owners who have held off over the past four months might start thinking about coming back to the market while there was still demand, TCorp chief economist Brian Redican said.

“Even if homeowners have accumulated a lot of equity and will not be selling for a loss, they could decide to sell later in the year if they are unable to keep meeting the mortgage repayments,” he said.

“This will start to increase supply. And that shifts the balance back to buyers.”

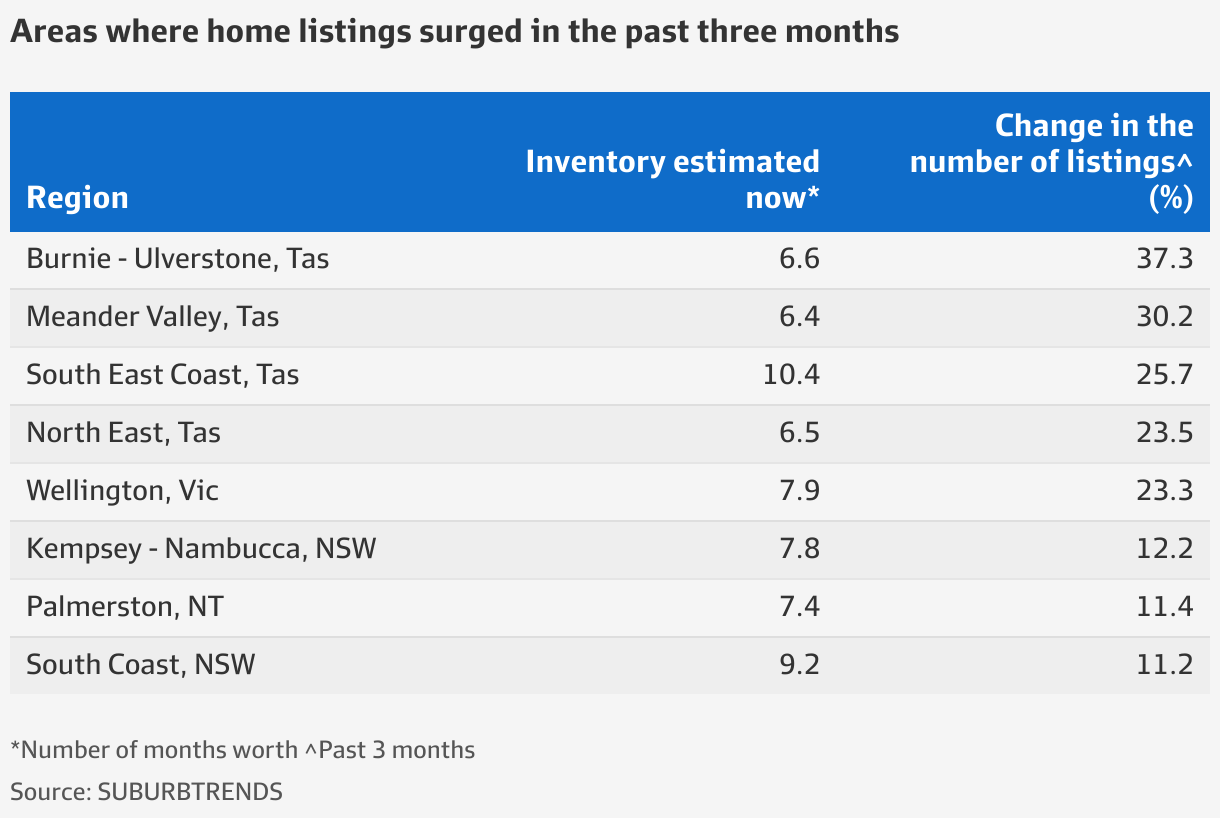

Some areas were already experiencing a substantial increase in house listings, fuelling a rise in inventory that exceeds six months, an indication of a slowing housing market, said Kent Lardner, founder of property data analytics Suburbtrends.

The South Coast in regional NSW and South East Coast in Tasmania posted the sharpest increase in inventory, estimated at 9.24 months and 10.35 months respectively, compared to 7.21 months and 6.60 months just three months ago.

Similarly, inventory across the Kempsey-Nambucca region in northern NSW and Wellington in Victoria has increased by more than two months to 7.79 months and 7.90 months respectively.

“Each of these areas is witnessing an upswing in listings and a notable rise in their estimated inventory levels when compared to three months ago, which is indicative of a slowing property market,” Mr Lardner said.

“This slowdown in demand is likely to apply downward pressure on property prices in the upcoming months.”