Let’s start with a bit of history. And to properly think about supply and demand in the housing market, you have to look at long runs of data, not just at a few years.

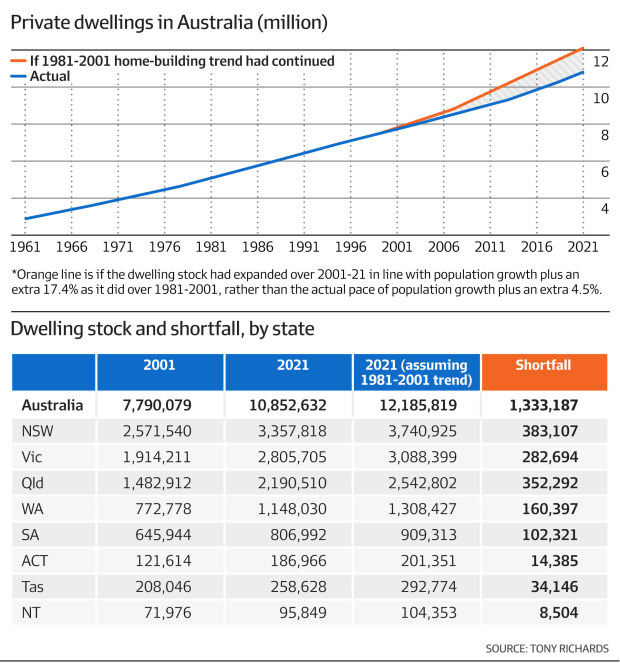

For many decades following the Second World War, the percentage growth in the number of homes was well in excess of the growth in the Australian population. At the 1981 census, the total number of private dwellings was 22 per cent higher than would have been implied just by the growth in the population since the 1961 census. In the 20 years to 2001, growth in the number of dwellings was 17 per cent higher.

Accordingly, that 40-year period saw a significant fall in average household size, that is, a fall in the average number of people per occupied dwelling. The drivers included both demographics, the trend towards smaller families, and preferences – as real incomes rose, people wanted more space.

But around the start of this century that changed. In the 20 years to 2021, the percentage growth in the number of dwellings was only slightly faster (by 4.5 per cent) than the growth in the Australian population, and the long-term downward trend in the average household size largely stopped.

This slowing in the growth of the housing stock was observed in all eight states and territories. If the relationship between the growth in the population and the housing stock seen in the 20 years to 2001 had been maintained over the 20 years to 2021, Australia would have had around 1.3 million more dwellings than the 10.85 million dwellings reported in the 2021 census.

The nation’s housing stock would have grown by around 220,000 dwellings per year over this 20-year period, rather than the growth of 153,000 per year that actually occurred.

The slowdown in the growth of the housing stock over the past two decades is surprising given that those earlier trends in demographics and preferences have surely persisted (and the pandemic will have added to these).

More broadly, there has been strong demand for housing, with financial liberalisation and lower interest rates significantly increasing household borrowing capacity, along with factors such as demand for housing for new short-stay rental models.

Tax policies are generally considered to have favoured ownership of housing. And state and federal governments have continued to provide assistance for first-home buyers.

Yet with all these factors boosting demand for housing, the past two decades did not see a continuation of the strong growth in the supply of housing that was seen in the four previous decades.

What we have seen instead is a significant increase in the price of housing, relative to household incomes (and even more so relative to the consumer price index). It is hard to escape a conclusion that the run-up in the price of housing over the past two decades must be related to inflexibilities in housing supply. Like all markets in the economy, the housing market has cleared.

However, the equilibrium that it has reached from the combination of strong demand and inflexible supply has been at much higher prices, with adverse effects on much of the population, both home buyers and renters.

What does economics tell us about urban structure and population growth? Of course, housing is an unusual market in many ways, with complex issues on both the demand and supply sides.

On the supply side, the complexities include that housing is a long-lived asset, that location is a key attribute, and that decisions about one person’s housing can affect their neighbour. So, there will inevitably be supply side challenges and building new housing is likely to get harder as our cities grow.

Theoretical models of urban structure can shed light on some supply side challenges. A 2011 Reserve Bank research paper that I wrote with Mariano Kulish and Christian Gillitzer highlights some key points.

We modelled the structure of cities that were calibrated to broadly match the attributes of Australia’s larger cities in terms of geography (a central business district, or CBD, close to the coast) and realistic assumptions about building costs, transport costs, and household incomes and preferences.

The model neatly demonstrated the key trade-off that households face in terms of choosing between smaller dwellings closer to the CBD or larger dwellings with longer commutes to the city centre.

Our model allowed us to look at the expected structure of cities under different assumptions about population size, urban planning rules, frictions in housing construction, and the cost of transport.

One particularly instructive exercise was to consider the equilibrium structure of two cities that differed only in population (two million versus four million) and otherwise had similar characteristics. The results of the simulation were mostly not surprising.

Because of more demand for housing, the city with the larger population had higher land and housing prices, smaller homes and higher population density. The larger population also resulted in the city growing outwards relative to the city with the smaller population.

But the surprising finding was how small this effect was. Indeed, although there were twice as many individuals living in the larger city of 4 million people, only about 1 per cent of those additional people lived outside the footprint of the city of 2 million people.

Now I understand that all models are approximations and contain simplifying assumptions. However, this comparison of the cities with 2 million and 4 million populations captures a key insight that we ignore at our peril.

As populations of cities grow, the natural tendency would be for most of that growth to be accommodated by greater density, rather than by growing outwards. That is, as the price of land rises, people adjust by economising on their use of land, by living in homes (either houses or apartments) that use less land per dwelling. Policies or institutional factors that have the effect of resisting these forces will be preventing many households from choosing the location and type of housing that best meets their preferences.

Of course, the adjustment of a smaller and lower-density city, with all its existing housing and infrastructure, towards a higher population and higher density is not easy. And our simulation did not attempt to model that adjustment – it was implicitly considering how a city might change if it could costlessly adjust.

Given that Australia is a highly urbanised country, and most of our population growth has been in our five large cities, it seems highly likely that the inflexibility of the supply side of the housing market of recent decades is related to problems that our cities have had in dealing with population growth.

The current planning process

Most would-be home builders would be unlikely to even begin on a planning proposal to secure a rezoning that would permit medium-density housing. Oscar Colman

Let’s now consider the way that the housing development process works (or doesn’t work) in Sydney, our largest city. There is a lot of talk about the “missing middle” in Sydney, that is the relative shortage of medium density housing, especially townhouses or low-rise apartments, relatively close to the city.

This is the type of housing that many households are interested in – from key workers to highly paid professionals, and from young people setting up households for the first time to downsizers who may want to stay in their existing neighbourhood but no longer want a freestanding house and its large garden. The Grattan Institute has done important work that clearly establishes the demand for such housing.

Suppose a home builder was keen to help supply new “missing-middle” housing, having observed that there was strong demand for medium-density housing in a particular area and there was also lots of land zoned for housing and currently in low-density usage.

Note that our building company could be wanting to build for the private market, for the build-to-rent sector or for affordable housing – local government approval processes will have to be met in all three cases.

Their first step would be to go to the website of the relevant local council to check on the rules for new development and the availability of appropriately zoned land in the local government area (LGA).

The council website would suggest that the building company should lodge a development application, unless their project is exempt or complying. To explore this, our prospective home builder would study the council’s Local Environment Plan (LEP), a document that is required by state legislation and is typically around 150 pages.

In addition, they would have to look at the council’s Development Control Plan (DCP), which contains much more detail regarding the development that the council will allow. It may be much longer – for example, Willoughby Council’s DCP is 751 pages in length, with an additional 204 pages of attachments.

The particular document that will be most relevant for our would-be home builder is the zoning map for the LGA. Our builder would no doubt find that there were large swathes of light-pink-coloured R2 (low-density residential) land, which essentially means it can only be used for single-family housing (with some small exceptions for dual-occupancies). And in some Sydney LGAs, there are also significant amounts of land zoned R1 (general residential) or C4 (environmental living), where new building is even more tightly controlled.

Our home builder would find much less land zoned for medium-density (R3) or other higher-density or more flexible uses. And they would soon discover that almost all of this land was already being used for medium- or higher-density housing, or was subject to other development proposals. So if our would-be home builder could not find any available land that was already zoned to allow new “missing-middle” housing, how would they go about getting a rezoning?

Rezonings can be one-off (or “spot”) rezonings in response to a particular planning proposal, or there may be some broader degree of rezoning around the major update of a council’s LEP. These major updates appear to occur about once a decade, after which zoning for the LGA will again be largely set in stone for another decade or so. The process for a spot rezoning is typically a long, difficult and uncertain one. It involves application fees, commissioning costly reports from various subject-matter consultants to support the application and the likely rejection of the application by council.

The applicant will then have to decide whether to attempt a costly appeals process that may bring in citywide or state-level bodies. If a rezoning is eventually achieved, there will then be a lengthy process of negotiation with council to get a development approval for a particular building design. The result is that most would-be home builders would be unlikely to even begin on a planning proposal to secure a rezoning that would permit the medium-density housing that there is strong demand for.

Instead, the way that development of medium-density housing often occurs is by developers/speculators trying to anticipate what rezoning might be feasible in future scheduled updates of LEPs, possibly a decade or more away. They will then buy up this land, or enter into options to buy the land, and then begin to try to influence the council planning process to include their land in a spot rezoning or in rezonings in future LEPs.

So, when you see a somewhat run-down house and garden in a well-located area that is close to transport, it is likely that it has been secured by a developer who is working on getting a rezoning and then a development approval. The costly and difficult current processes around planning proposals and rezonings have unfortunate implications.

The upshot is that the important tasks of home building and modernising our cities have become heavily reliant on individuals and firms whose main skill is navigating the development approval process and influencing local and state government officials to try to ease constraints on what can be built.

Our current arrangements introduce barriers to entry and add significantly to the cost of home building relative to a more open process. Needless to say, they are also prone to corruption at the local and state government levels.

Some possible solutions

Councils in Sydney’s inner and eastern suburbs are allowing hardly any new construction. Brook Mitchell

If we care about housing affordability and having a city that better meets the housing needs of its population, we need planning and zoning arrangements that allow our cities to adjust more easily.

We need a planning and approvals system that is easier for home builders to interact with, rather than one that is complex, expensive and corruption-prone. We need a system that allows the construction of a housing stock that suits today’s needs and future needs and is not largely set in stone based on building or planning decisions made 20 or 50 or 100 years ago.

To be clear, I am talking about how to make better use of land that is already zoned residential. This is not about taking over parkland or land currently used for community and recreational use. And I am not talking about forcing redevelopment, but rather about not preventing it if there is indeed significant demand for new and different types of housing to better suit current and future housing needs. And my focus is on medium-density housing as opposed to high-rise housing, which our system has arguably over-delivered on.

Let’s start by pointing out some charades in current local planning processes. One element of the current process is that local councils in Sydney are each required to produce a local housing strategy (LHS) that supposedly takes account both of demand and supply factors in their LGA as well as objectives for Greater Sydney such as greater housing supply and a more diverse and affordable housing stock.

The first step for some local councils appears to be to start with population growth forecasts for their LGA that assume very little growth (or sometimes even declines) in population and are presumably premised on very limited change in zoning and development policies. Based on the apparent limited need to house additional people, the council then produces an LHS (and presumably, subsequently, an LEP and DCP) that allows only very limited development and accommodates only a modest increase in population. Talk about conclusions flowing directly from the assumptions.

An extreme example of this process was the 2021 LHS for Hunters Hill, a relatively low-density LGA that is just six kilometres from Sydney’s GPO, which based its LHS on a projection that its population would actually fall in the 20 years to 2036.

As many others have argued, building more medium-density housing may require taking some powers out of the hands of local councils and having decision-making that looks beyond the preferences of current residents, including NIMBYs, and more to the needs of the broader city and of future generations of potential residents. Peter Tulip has written about this recently.

One modest step towards holding local councils accountable would be for the publication of continually updated maps showing actual development capacity in each LGA, as opposed to just maps with zoning but without information about current land use.

The Department of Planning and Environment could publish (or require councils to publish) maps showing all land that genuinely has capacity for additional medium-density housing – i.e. land zoned R3 or R4 (or mixed use) that is not currently close to its development capacity, not already subject to a development application, and not subject to any practical hindrances to building more housing.

Local councils could also be required to ensure that there is a certain amount of development capacity available at all times, say in terms of the net increase in homes that would be feasible.

If there was demand for additional housing in the LGA and the developable land was being used up, councils would then have to rezone additional developable land and ensure that it published a timely and accurate indication of the scope for building additional housing in the LGA. This could ensure that all LGAs were “pulling their weight” in allowing for the provision of new housing.

If such a measure was not effective, it might become necessary to consider stronger measures, such as the broad-based elimination of low-density zoning as occurred in Auckland in 2016. Around three-quarters of the Auckland suburban area was up-zoned and single-dwelling zoning restrictions were removed. The evidence suggests that those reforms have been effective in encouraging housing construction and holding down housing prices, and they apparently have had quite broad support from the population.

Or perhaps there could be an automatic right to build R3-compliant housing anywhere that a home builder has been able to consolidate a certain quantity of contiguous R2-zoned land.

Alternatively, it might be possible to use price-based incentives around a broad-based land tax to encourage local councils to allow more construction of medium-density housing in their LGAs.

There are very good reasons from a macroeconomic perspective to replace transaction stamp duties with a broad-based land tax applying regardless of whether the land is used for owner-occupied or rental property.

And a land tax is also attractive from a more microeconomic perspective in encouraging the efficient use of land. For example, as annual land tax can encourage older households with larger homes than they need to sell to younger and larger households and to downsize to housing that is actually better suited to their needs.

A standard broad-based land tax could be modified so that any land that was zoned for low-density use (R1, R2, C4, etc) was taxed based on the value it would have if it were zoned for medium-density use. The effect would be to increase the land tax levied on low-density-zoned land close to the CBD that would be suited for medium-density housing. In contrast, less-well-located land that was not attractive for medium-density use would not see an uplift in its land tax.

A land tax along these lines could have two benefits. First, it could raise revenue that could be used to offset the negative externalities that arise when land that is well suited for medium-density use is not available for such use. Second, because residents with well-located land close to the CBD would face an annual land tax obligation that reflected the development potential of their land regardless of its zoning, it could counter the incentive for NIMBY residents to oppose zoning that would permit use for medium-density housing.

‘No-one wants to live in apartments’

Most of the cities that Australians – including those living in our affluent, low-density suburbs – love to visit have much more medium-density housing than Australian cities. Bloomberg

There are of course some in the community who oppose any suggestion about building more medium-density housing in our inner- and middle-ring suburbs. Any time that an article along these lines is published in a major newspaper there are all sorts of outraged responses.

Many of these are essentially people trying to impose their own views or tastes on others. There are the incorrect assertions about housing demand (e.g. “no-one wants to live in apartments”) or about supply (e.g. “all apartments are poky and small”). And there are also the let-them-eat-cake responses.

We should reject these responses. Australian cities have much lower density than large cities in most other higher-income economies. For example, most of the attractive European cities that Australians – including those living in our affluent, well-located and low-density suburbs – love to visit have much more medium-density housing than Australian cities.

And there are already parts of Sydney which show that three- or four-storey apartments, when done well, can be very attractive. And it is more likely that they will be done well when there is a range of sites available to builders when they are considering how they can best meet the demand for missing-middle housing. If we make it easier to build medium-density housing, we will presumably get a wider range of such housing to cater to all segments of the market.

The need for reforms on other fronts

Of course, my focus on the supply side should not be interpreted as a silver bullet for all Australia’s housing issues. There is scope for separate and complementary policy action on several other fronts:

- Greater assistance for lower-income renters, including more provision of social and affordable housing, is certainly also needed. The run-up in the cost of housing (both owner occupied and rented), plus the significant decline in the share of public housing in the overall housing stock over the past few decades, has resulted in significant housing issues for lower income groups.

- Greater investment in transport infrastructure can make it more attractive to live further from CBDs, including in nearby centres outside the major cities.

- The removal of any unwarranted tax impediments to the corporate provision of build-to rent housing.

- There may also be a case for reforms to the personal tax treatment of both owner-occupied and investor-owned housing. However, I would suggest that we should be wary of excessively demonising property investors. There will always be a significant fraction of the population who prefer to rent and have no interest in buying, and we rely on investors to provide that part of the housing stock that will be occupied by those renters.

- And yes, some people will argue that we need to have a debate about immigration and population growth. However, we have a significant undersupply of housing for our existing population that needs to be resolved. Any debate about population growth should not be allowed to stop sensible measures to deal with those housing problems that currently exist for the existing population because of various policy failures of recent decades.

Finally, it should not need repeating, but we should be wary of band-aid demand-side policy responses to problems of housing affordability and availability. As I said in a speech in 2008, “it is now widely accepted that policies that simply give people more money to spend on housing are likely to be capitalised into higher housing prices”.

Unfortunately, over the past couple of decades, politicians have too frequently responded to housing problems with policy measures that allow a particular group of people to spend more on housing, which inevitably worsens the affordability problems for others who do not benefit from those policies.

The benefits of reform

Countless reports in recent years have called for action on the supply side of our housing market. If we remove frictions that are reducing supply, we should see increased home building that over time will help to make housing more affordable, for both owner occupiers and renters.

With significant rezonings in the inner and middle rings, land for medium-density housing would be less costly than currently. Together with home builders facing fewer hoops to jump through in getting planning proposals approved, more housing could be built and sold at lower prices than under the current system.

Of course, the removal of these frictions will take time to have a material effect – the current affordability problems are the result of developments over decades and will not be unwound in just a few years. But regardless of whether the benefits in terms of affordability are significant or only modest, we should make it easier for our cities to evolve and grow.

Greater flexibility on the supply side of the housing market will help to make our cities work better and improve Australia’s productivity. Quite simply, we need reforms that allow people to live in housing that works better for them.

Tony Richards is chairman of the steering committee for the central bank digital currency project at the Digital Finance Cooperative Research Centre. He previously held senior roles at the Reserve Bank of Australia including head of economic research, head of economic analysis and head of payments policy.

Read more about the housing crisis

- Councils, NIMBYs to blame for 1.3m missing homes The homes were not built over the past 20 years chiefly due to costly zoning, planning and building red tape imposed by local councils who are worsening the nation’s housing shortage, according to new research by former RBA economist.

- No more homes, no cafe, no fun. Meet Sydney kill-joy suburb For almost a decade, Charlie Colosi has tried to turn an abandoned colonial-era asylum into a thriving restaurant that would breathe life into a dull corner of privileged Sydney. For much of the time, Hunters Hill Council has resisted him.

- House prices are going back up Later week, Core Logic data will show that the third consecutive month, national property prices have increased, and this time at a rate that exceeds the previous two months.